- Who gains when interest rates fall? [pdf]

with Max Miller, James Paron and Natasha Sarin

Reject & Resubmit at the American Economic Review

We study the interest-rate sensitivity of household wealth in a realistic life-cycle model. The model predicts that middle-aged and wealthier households should hold more long-term assets, as observed in the US data. Consequently, optimal portfolio rules imply that falling interest rates increase wealth inequality, while rising rates reduce inequality, consistent with historical experience. However, these long-run shifts in wealth inequality are largely offset by changes in the valuation of human capital and Social Security benefits, mitigating the passthrough of interest-rate fluctuations to expected lifetime consumption.

- Robustness Checks in Structural Analysis [pdf]

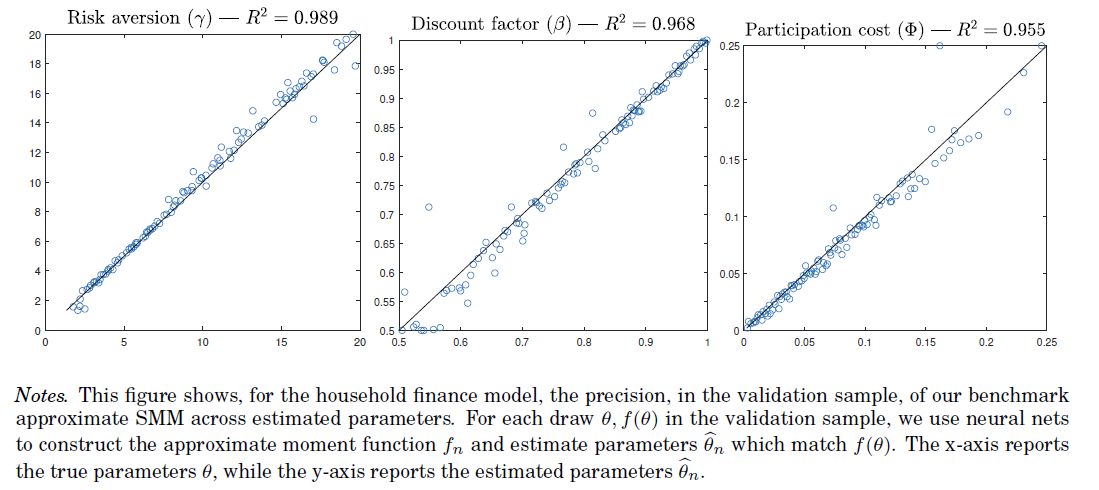

with Mehran Ebrahimian, Mohammad Fereydounian, David Sraer and David Thesmar

This paper introduces a computationally efficient methodology for estimating variants of structural models. Our approach approximates the relationship between moments and parameters, offering a low-cost alternative to traditional estimation methods. We establish general convergence conditions, primarily requiring model-based moments to be continuous functions of parameters. While this continuity does not necessitate a continuous economic model, it does require the model to have only sparse discontinuities, a concept we define. We also provide convergence rate bounds for Kernel and Neural Net approximations, with the latter demonstrating superior performance in higher dimensions.

We apply this methodology to two standard structural models: (1) dynamic corporate finance and (2) life-cycle portfolio choice. We demonstrate the reliability of our approach through simulations and then use it to explore identification, robustness to sample splits and moment selection, and model misspecification. These explorations are computationally infeasible with standard techniques, but become trivial with our methodology.

Performance of SMM Approximation using neural nets — household finance model

- Labor Market Risk and the Private Value of Social Security [pdf]

Social Security provides insurance against idiosyncratic income risk but exposes workers to systematic risk because benefits are indexed to the evolution of aggregate earnings. I calibrate a life-cycle model to compare workers’ certainty equivalent valuation of Social Security to its net present value discounted at the risk-free rate. I show that, overall, labor market risk reduces current workers’ private value of Social Security by 46%. This adjustment sums up to $11.4 trillions on the national scale and the equity premium is its main determinant. For workers under 30, the certainty equivalent of Social Security is negative. Exposure to systematic risk through Social Security peaks relatively late in the life-cycle.